Menu

✕

June 2, 2026>Board360

QUICK ANSWER: For most Indian candidates with no prior US tax experience: Part 3 first (easiest, highest pass rate), then Part 2, then Part 1. For those working in US individual tax: Part 1 first. The optimal order depends on your background, not a universal rule.

The three parts of the Special Enrollment Examination can be taken in any order, in any combination, within a single testing window. That flexibility is powerful, but it also creates a decision that many Indian candidates overthink.

The right order is not the same for everyone. This post gives you the pass rate data, a clear breakdown of what each part actually tests, honest difficulty ratings by candidate background, and a sequence recommendation based on your specific profile.

An important caveat from Prometric itself: direct comparison of pass rates across the three parts is not straightforward, because nearly twice as many candidates sit Part 1 as sit Parts 2 or 3. Many who fail Part 1 stop there and never sit the other parts, which depresses Part 1's pass rate for structural reasons, not necessarily because the content is harder.

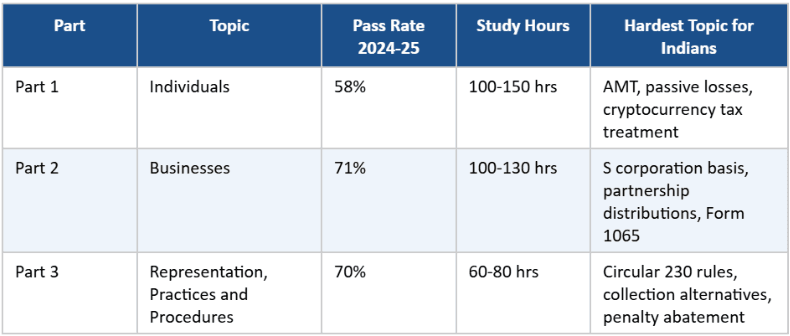

Part 1 covers US individual income tax. The broad topics are: income and assets, deductions and credits, and specialized topics including estate and gift tax.

The content that trips up Indian candidates is not the straightforward income reporting. It is the complexity layered on top: passive activity loss rules, alternative minimum tax (AMT), earned income tax credit phase-outs, cryptocurrency tax treatment, net investment income tax, and the interaction between various deductions and AGI thresholds. These are areas where a simple reading of the Form 1040 does not prepare you.

Part 1 also now includes implications of the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025. New provisions including the no-tax-on-tips deduction, no-tax-on-overtime deduction, the raised standard deduction, the higher SALT cap, and the new $6,000 senior deduction are testable in Part 1 from the September 2026 testing window onwards for international candidates. Ensure your study materials are updated to reflect these changes.

Study hours recommended: 100 to 150 hours. Candidates with a background in US individual tax preparation can potentially reduce this. Candidates new to Form 1040 content should not go below 100 hours.

Part 2 covers US business taxation: corporations (C corps and S corps), partnerships, estates, trusts, and retirement plans. It tests three domains: business entities, business financial information, and specialized returns.

Part 2 has the highest pass rate of the three parts at 71%. But do not take this as a signal that it is easy. Historically, Part 2 had the lowest pass rate. The improvement is attributed to candidates now approaching Part 2 with more preparation and with the experience of having sat at least one other part first.

For Indian CAs and accounting graduates, Part 2 has the most conceptual overlap with existing knowledge. Corporate taxation structures, entity-level income allocation, and basis concepts align with Indian accounting education in ways that individual US tax does not. This is why many Indian preparation providers recommend Part 2 as a strong second part for accounting-background candidates.

The areas Indian candidates find hardest in Part 2 are S corporation shareholder basis tracking, partnership distribution rules under Sections 731 to 736, and the nuances of Form 1065 reporting. These are structural concepts that require systematic study rather than experience-based familiarity.

Study hours recommended: 100 to 130 hours. Candidates with corporate accounting experience can target the lower end.

Part 3 covers IRS procedures, ethical standards, and EA representation rights. The three domains are practices and procedures, representation before the IRS, and specific types of representation.

Part 3 has the most consistent pass rate year over year, hovering at 70% for several consecutive testing windows. It is widely regarded as the most accessible of the three parts, primarily because:

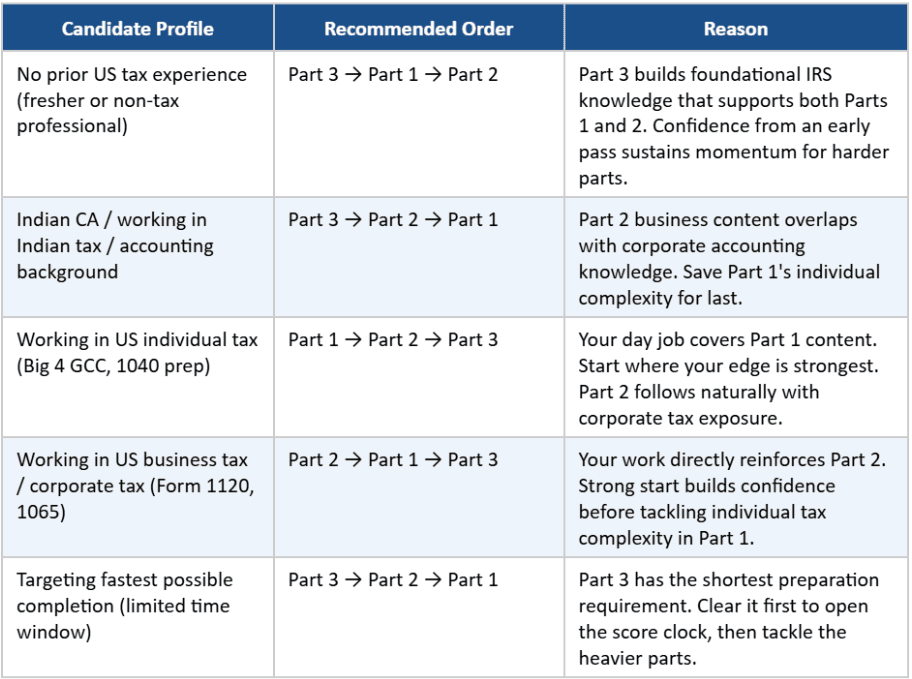

For Indian candidates with no prior US tax background, Part 3 is the recommended first attempt. Clearing it early builds IRS procedural knowledge that provides useful context when studying Parts 1 and 2. It also puts a passed section on your record, which opens the scoring window and provides confidence for the more difficult content ahead.

Study hours recommended: 60 to 80 hours. This is substantially less than Parts 1 and 2, which is why starting with Part 3 allows you to accumulate an early pass relatively quickly.

There is no single correct order. The right sequence is determined by your background, your current role, and how much preparation time you have before your testing window.

The most commonly recommended sequence for Indian candidates without prior US tax experience is Part 3 → Part 2 → Part 1. Part 3 provides an early win and foundational IRS knowledge. Part 2 leverages accounting background. Part 1 is tackled last with momentum, experience, and the widest body of study support behind you.

Failing a part is not the end of your EA journey. The IRS allows up to four attempts per part per testing window. The international testing window for Indian candidates (September 1, 2026 to February 28, 2027) gives you approximately six months in which you can retake a failed part.

There is a 24-hour waiting period before you can rebook the same part after a fail. There is no waiting period before sitting a different part. So if you fail Part 1, you can sit Part 2 the next day if you have it scheduled, and return to Part 1 after reviewing the diagnostic report you receive at the testing center.

The diagnostic report is one of the EA exam's most useful features. Failing candidates receive a section-by-section performance breakdown immediately at the end of their exam session. This tells you exactly which topic domains you underperformed in, allowing you to target your retake preparation precisely rather than restudying everything.

Each retake costs the full exam fee of $317. This is a real cost, but it is not a reason to delay sitting. The cost of postponing your EA journey by three to six months while waiting for certainty is typically higher than the cost of one retake fee.

Yes. The international testing window (September 1, 2026 to February 28, 2027) is approximately six months. Three exams across six months is an achievable pace for well-prepared candidates.

The typical cadence for candidates completing all three parts in one window is roughly six to eight weeks per part. Sitting Part 3 in September, Part 2 in November, and Part 1 in January or February is a realistic and commonly used schedule.

A word of caution: do not let the six-month window create a false sense of pace. Cramming all three parts into a short period with insufficient preparation time is a false economy. Failing a part and retaking it is more disruptive than allowing an extra four to six weeks of preparation between parts on a first attempt.

Board360.ai's EA program, powered by HOCK International, covers all three parts with adaptive practice banks, section-specific mock exams, and OBBBA-updated content for Parts 1 and 2. Explore the EA program at Board360.ai to understand the study structure before planning your sequence.

The EA exam is scored on a scale of 40 to 130. The passing score is 105. When you pass, you are simply told you passed. When you fail, you receive your scaled score and the diagnostic breakdown.

In practice, candidates whose mock exam performance consistently sits at 65% correct or above across a full 100-question practice paper are typically ready to sit. Candidates who are consistently at 55 to 60% on practice papers benefit from another two to three weeks of targeted study before sitting, particularly on the specific domains where the diagnostic pattern shows weakness.

The scaled scoring means you cannot map percentage correct to scaled score precisely. A 70% raw score on a harder exam version might scale to a higher result than a 75% raw score on an easier version. Focus on demonstrated mastery and consistent practice performance, not on hitting a specific percentage target.

Board360.ai's Enrolled Agent program is powered by HOCK International, with a 95% pass rate across all three parts. The program covers Part 1 with OBBBA-updated content, Part 2 with full corporate and partnership tax coverage, and Part 3's procedural and ethical framework. A free demo is available. Explore the EA program at Board360.ai and start with the part that best fits your background.