Menu

✕

June 6, 2026>Board360

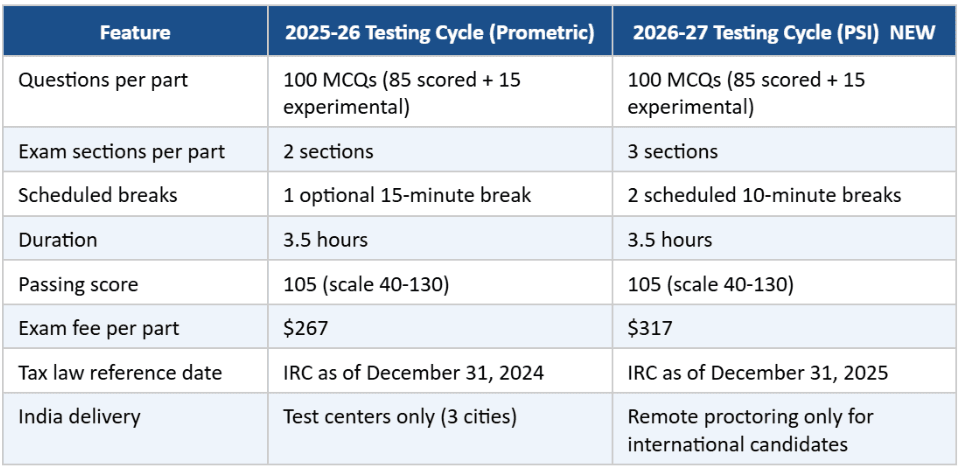

QUICK FACTS: 100 MCQs per part. 85 scored + 15 experimental. 3.5 hours. Passing score: 105 of 130. Tax law reference: IRC as of December 31, 2025 for the September 2026 window. NEW in 2026: 3 exam sections per part, 2 scheduled 10-minute breaks.

Knowing the syllabus is not the same as knowing what to prioritize. The EA exam tests you on 300 questions across three parts, but the questions are not evenly distributed. Each part has three or five domains, each with a different weightage. Study time allocated proportionally to that weightage is study time spent correctly.

This post gives you the full domain breakdown for all three parts, with approximate weightages, the specific topics within each domain that Indian candidates find most challenging, the 2026 format changes you need to know, and a direct comparison to CPA REG for candidates evaluating both credentials.

The IRS Candidate Information Bulletin for the 2026-2027 cycle introduced several structural changes alongside the vendor switch from Prometric to PSI Services. The syllabus domains and weightages are unchanged, but the exam-day experience is different. Candidates sitting from September 2026 need to know these changes.

The most practical change for Indian candidates is the break structure. The previous single optional break has been replaced by two scheduled 10-minute breaks within the 3.5-hour session. The exam is now split into three sections. Use the breaks deliberately. After completing the first section, take the break even if you feel confident. Mental fatigue accumulates invisibly across 100 questions.

The tax law reference date matters for study materials. For the international window (September 1, 2026 to February 28, 2027), all questions reference the Internal Revenue Code as amended through December 31, 2025. This includes OBBBA provisions signed July 4, 2025. Ensure your study materials and question banks are updated to reflect law as of December 31, 2025, not December 31, 2024.

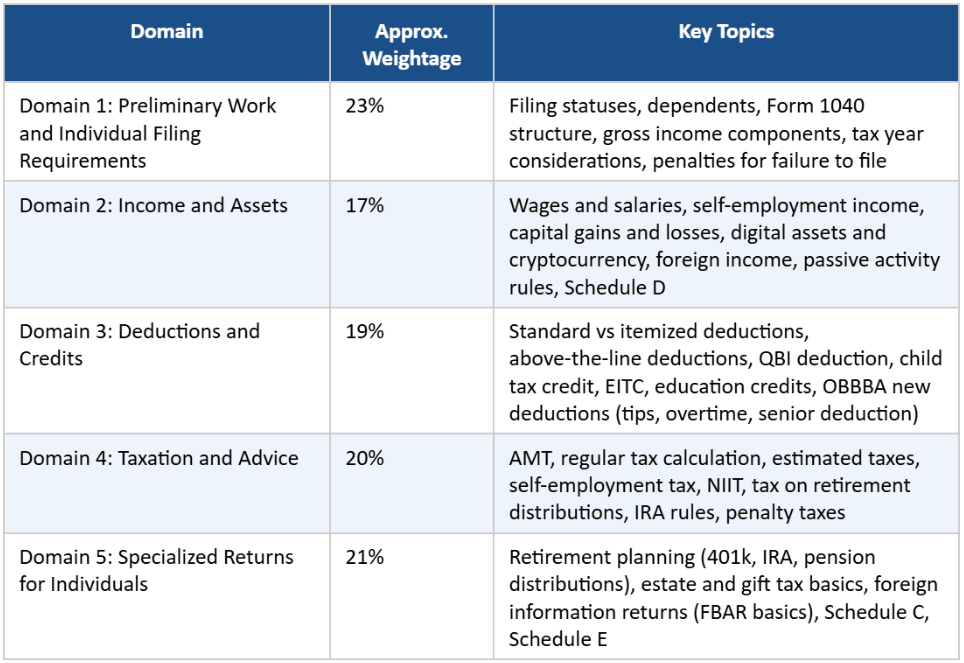

Part 1 covers US individual income taxation. It is the broadest in topic range and the part that Indian candidates with no prior US tax exposure find most unfamiliar. The five domains and their approximate weightages are drawn from the IRS Content Specification Outline published annually in the Candidate Bulletin.

Key study points for Indian candidates:

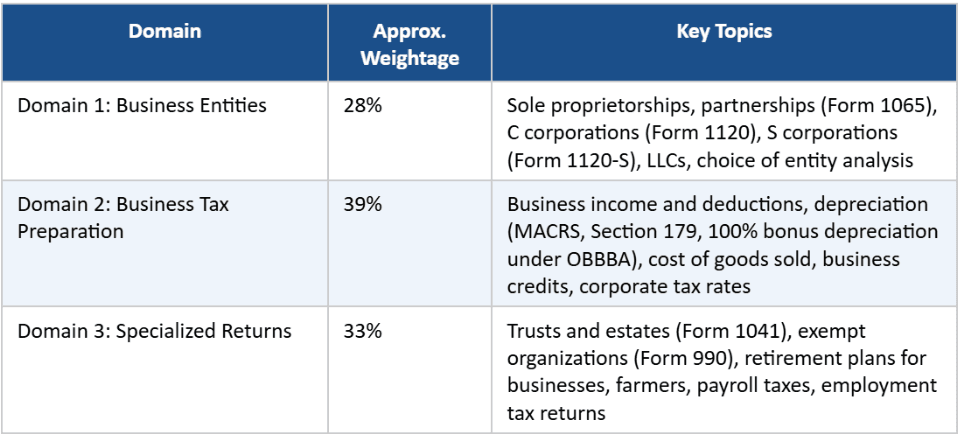

Part 2 covers US business taxation. It has the highest pass rate of the three parts (71% in 2024-25), but it is considered 'The Beast' by preparation providers because the entity-level tax rules require understanding structural differences between C corps, S corps, and partnerships.

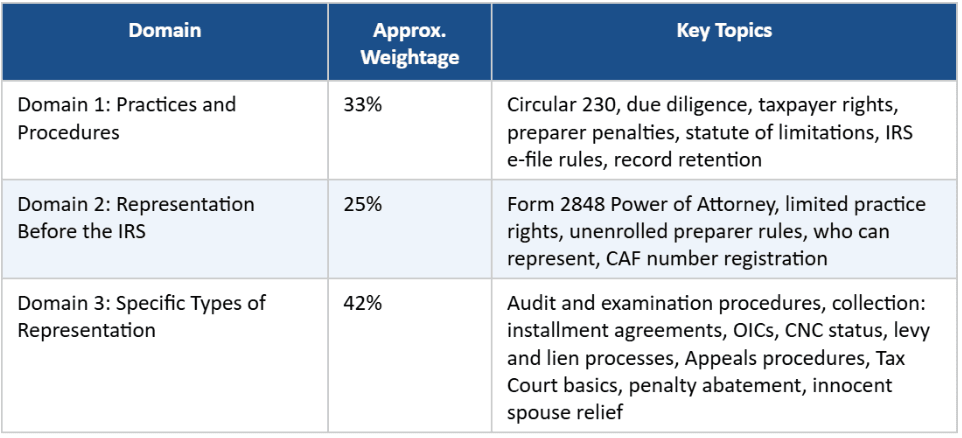

Part 3 is the most accessible part for most candidates and the one that most directly validates the EA's distinctive value: the legal right to represent taxpayers before the IRS. It is procedural and rule-based rather than computational.

Key study points for Indian candidates:

The domain structure and weightages are unchanged from the prior cycle. The IRS reviews the content specification annually but changes are typically minor and gradual. The same five domains for Part 1, three domains for Part 2, and three domains for Part 3 that have been in place for several cycles remain in effect.

What has changed in 2026 is the tax law reference date and the OBBBA provisions. For the September 2026 international window, the exam references the IRC as of December 31, 2025. This means OBBBA provisions signed July 4, 2025 are fully testable.

The specific OBBBA content that is new for the September 2026 window includes: permanent 100% bonus depreciation, Section 179 limit raised to $2.5 million, permanent TCJA individual tax brackets, no-tax-on-tips deduction (2025-2028), no-tax-on-overtime deduction (2025-2028), raised SALT cap ($40,000), increased Child Tax Credit ($2,200), senior additional deduction ($6,000 for age 65+, 2025-2028), and auto loan interest deduction ($10,000, 2025-2028).

Confirm that your study materials reflect these OBBBA changes before sitting. Board360.ai's EA program, powered by HOCK International, maintains current content alignment with each testing window. The HOCK program is updated to reflect the December 31, 2025 law reference for the international testing window starting September 1, 2026.

Study hours vary by candidate background. These ranges apply to Indian candidates with an accounting or finance background:

Total across all three parts: 260 to 360 hours. At 2 focused hours per day, that spans 5 to 6 months. Candidates with prior US individual or business tax experience can reduce Parts 1 and 2 study hours by 20 to 30 percent.

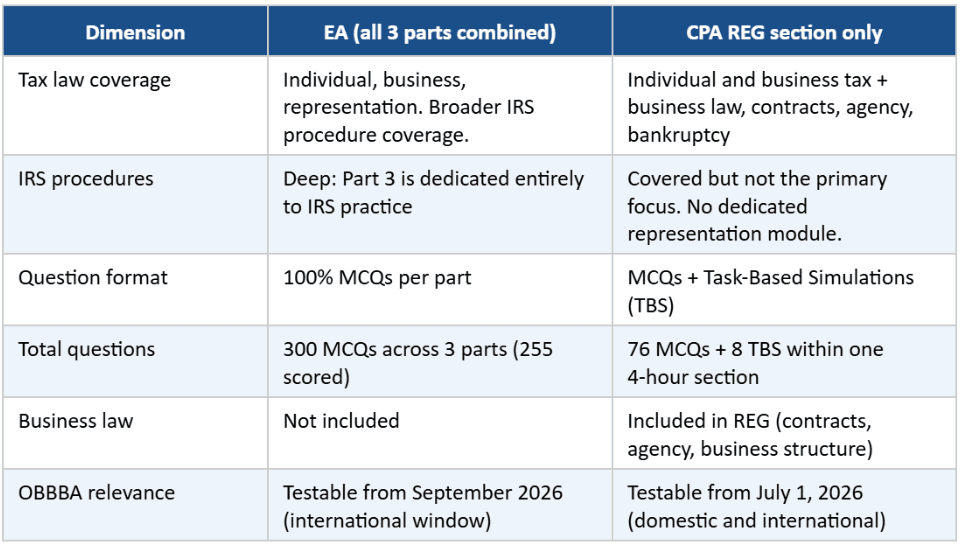

Many Indian candidates compare the EA to the CPA and want to understand how the tax content overlaps.

The EA covers more IRS procedure than CPA REG. If your career goal is IRS representation and US tax practice, the EA's three-part structure covers that domain more thoroughly. If your goal is the full public accounting credential with audit, tax, and advisory scope, the CPA covers a wider terrain but goes less deep on IRS-specific procedures.

Board360.ai's EA program is powered by HOCK International, with a 95% pass rate across all three parts. The program is fully updated to the December 31, 2025 tax law reference for the September 2026 international window, including all OBBBA provisions. Adaptive practice questions, part-specific mock exams, and expert faculty support are all included. A free demo is available. Explore the EA program at Board360.ai and start your preparation with materials built for the testing cycle you will actually sit.