Menu

✕

June 2, 2026>Board360

SHORT ANSWER: Yes, an EA in India can represent US clients before the IRS remotely. The EA holds unlimited representation rights under Circular 230 — the same rights as a US CPA or tax attorney. The legal instrument is Form 2848, IRS Power of Attorney. No geographic restriction applies.

Most discussions of the EA credential focus on tax preparation. That is only half the picture. The credential's defining feature is not what an EA can prepare. It is what an EA can do after the return is filed, or instead of filing, when something has gone wrong.

IRS representation is the work that separates an EA from any other tax professional in India. An unenrolled tax preparer in India can prepare and file US returns. Only an EA, CPA, or tax attorney can formally stand in for a US taxpayer before the IRS, communicate on their behalf, negotiate their tax liability, and represent them in audits and appeals. This post explains what that work actually looks like, how it flows from India, and why it represents one of the highest-value services an Indian EA can offer.

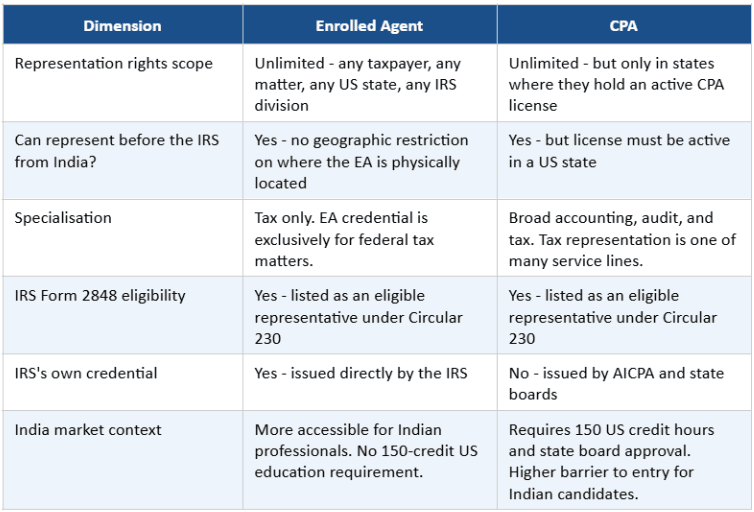

The phrase 'unlimited representation rights' comes from IRS Circular 230, the federal regulation governing tax practice before the IRS. Under Circular 230, three categories of practitioners hold unlimited representation rights: attorneys, CPAs, and Enrolled Agents.

Unlimited means exactly that. An EA can represent any taxpayer, on any tax matter, before any division or office of the IRS, in any US state. There is no restriction by geography, taxpayer type, tax year, or matter type. The EA credential is issued directly by the IRS, which means it is recognized by the IRS in all its offices and divisions without state-level qualification requirements.

Compare this to an unenrolled tax preparer: they can only represent taxpayers for returns they personally prepared and signed, and only during examination of those specific returns. They cannot represent in collection matters, appeals, or any other IRS proceeding. An EA faces none of those restrictions.

The practical significance for Indian EAs is that the geographic location of the EA is irrelevant. An EA sitting in Bangalore or Hyderabad holds the same representation rights before the IRS as an EA sitting in New York. All IRS communication can be handled by email, fax, phone, and the IRS e-services portal. No physical presence in the US is required for any IRS representation matter.

Before an EA can communicate with the IRS on a client's behalf, the client must execute IRS Form 2848, Power of Attorney and Declaration of Representative. This form is the legal instrument that authorizes the IRS to communicate with the EA rather than with the taxpayer directly.

Form 2848 is specific. The taxpayer defines the scope of the EA's authority by listing the tax matter type (income, employment, excise), the relevant IRS form (1040, 1120, 1065), and the applicable tax years. The EA cannot act outside those defined parameters without a new or amended 2848.

Once filed, Form 2848 authorizes the EA to receive and inspect the taxpayer's confidential tax information, communicate with IRS examiners, negotiators, and appeals officers, submit documents on the taxpayer's behalf, and act on any matter covered within the 2848's defined scope.

There is no expiry date. A Form 2848 remains in effect until the taxpayer revokes it, the EA withdraws, or a new 2848 is filed that supersedes it. The form can be signed electronically by the taxpayer under IRS e-signature rules, which means an Indian EA working with a US client never needs a physical document.

Form 2848 can be submitted online through the IRS's Tax Pro Account system, by fax, or by mail. The online submission path is the fastest and most reliable for practitioners working remotely from India.

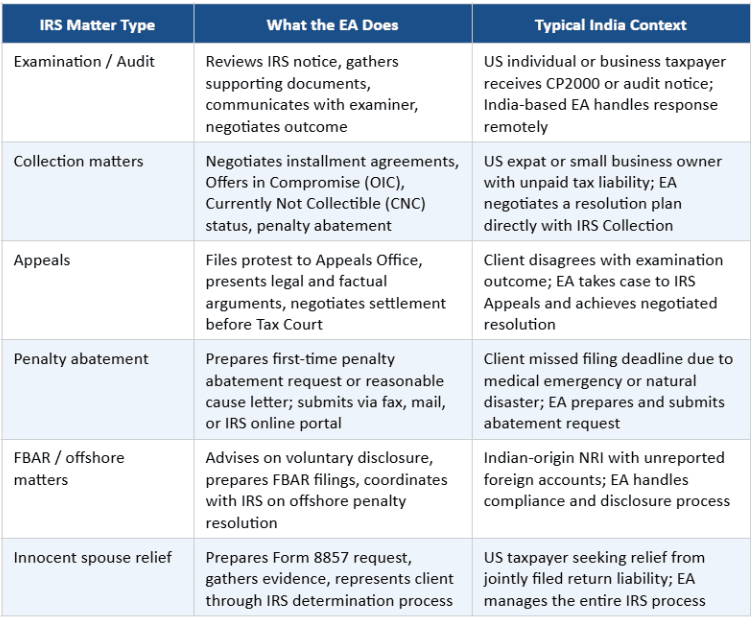

Here is what the work actually looks like across the most common IRS representation matter types.

The most common matter type for India-based EAs working with US CPA firms is examination response and collections. Individual US taxpayers receive CP2000 notices, under reporter notices, and examination letters regularly. A US CPA firm that outsources return preparation to an India-based team can also outsource notice response and examination correspondence to an India-based EA, who handles the full cycle from receipt of notice to IRS resolution.

An IRS audit, formally called an examination, follows a predictable sequence. Understanding this sequence is the foundation of effective audit representation.

It begins with the notice. The IRS issues an examination notice specifying the tax year under review, the items being questioned, and the deadline for response. The EA's first action upon receiving the case is to review the notice carefully, identify exactly what is being questioned, and pull the original return and all supporting documentation.

The EA then files Form 2848 if not already on file, which authorizes the IRS to communicate with the EA rather than the taxpayer. The examiner shifts all correspondence to the EA's contact information from that point.

The EA gathers documentation: bank statements, receipts, employer letters, or whatever the IRS is questioning. They organize the documentation in IRS-compatible format and prepare a response that addresses each item in the notice. The response goes to the examiner by the deadline, along with the supporting documentation.

If the examiner accepts the documentation, the case closes with no change. If the examiner disagrees, the EA can request a meeting with the examiner's supervisor or elevate the matter to IRS Appeals. Throughout this process, the taxpayer never needs to speak with the IRS directly. The EA manages every touchpoint.

For India-based EAs, the entire process runs remotely. Examiners accept responses by fax, mail, and the IRS e-services portal. Conference calls with examiners can be held by phone. No in-person attendance is required for correspondence examinations, which represent the majority of individual audits.

The key difference for Indian professionals is accessibility. Both credentials confer the same unlimited representation rights before the IRS. But the CPA requires 150 US credit hours and state board approval — a more complex path for an Indian candidate. The EA requires passing three SEE parts, which most accounting-background candidates complete in 10 to 20 weeks. For an Indian professional whose career goal is US tax and IRS representation specifically, the EA is the more direct route to those rights.

Yes, without qualification. The IRS does not restrict representation by geography. Circular 230 applies to practitioners regardless of where they are physically located, and IRS representation has been conducted remotely by practitioners outside the US for many years.

All major IRS channels are accessible remotely: the IRS e-services portal, the Tax Pro Account system for POA submissions, fax correspondence with IRS divisions, phone contact with collections and examination officers, and the Electronic Account Resolution system for account-level inquiries.

The only IRS proceeding that traditionally required physical presence was Tax Court litigation. Even that has shifted substantially since 2020. IRS Appeals conferences are now routinely conducted by video or phone. Collection Due Process hearings can be held telephonically. For an India-based EA, the practical constraints of remote representation are minimal.

There is no standard fee schedule. IRS representation is billed based on matter complexity, the EA's experience level, and the client relationship.

For India-based EAs working with US CPA firms on an outsourced basis, hourly rates for representation work typically run between USD 25 to USD 60 per hour, with experienced EAs specializing in collections or appeals commanding the higher end. At 40 to 50 billable hours per month, a productive India-based representation EA can generate USD 1,200 to USD 3,000 per month from a single US firm relationship.

For EAs working directly with US clients, fee structures are typically matter-based rather than hourly. A penalty abatement request for a first-time penalty might be billed at USD 300 to USD 600. A CP2000 notice response might be USD 500 to USD 1,500. A full correspondence audit representation engagement might be USD 1,500 to USD 5,000 depending on complexity.

Offer in Compromise (OIC) cases, where an EA negotiates a taxpayer's total IRS liability down to a reduced lump sum, are typically billed at USD 3,000 to USD 7,500 as a flat fee. OICs are complex, time-intensive engagements that require deep knowledge of IRS collection standards and financial analysis.

This is one of the most underutilized income opportunities available to Indian EAs.

US CPA firms that outsource return preparation to India frequently also have representation work they cannot handle in-house during peak periods. An EA in India who has demonstrated competency in notice response and audit correspondence is a natural fit for this overflow. Many US firms are actively looking for India-based EAs who can handle examination correspondence, penalty abatement requests, and installment agreement negotiations on a per-matter basis.

The freelance path requires two things beyond the EA credential: experience in US tax practice at the level needed to understand the underlying tax issues in each matter, and a working knowledge of IRS procedures and communication channels. Most EAs who move into freelance representation have 2 to 4 years of salaried experience in US tax roles first, which provides the foundation to handle representation matters independently.

Platforms like Upwork host active listings from US CPA firms seeking EA-level contractors for representation work. LinkedIn outreach to US CPA firm partners who work with Indian tax teams is the other reliable acquisition channel. The work is highly recurring: a US client who has an audit handled well will return for every subsequent IRS matter, and will typically refer to other US taxpayers in their network.

IRS representation is available only to credentialed practitioners. Board360.ai's Enrolled Agent program, powered by HOCK International, covers all three SEE parts including Part 3's Representation, Practices and Procedures module in full depth, equipping you with the practical knowledge of IRS procedures, Circular 230, and Form 2848 that representation work requires. The program has a 95% first-attempt pass rate. A free demo is available. Explore the EA program at Board360.ai and start building the credential that makes IRS representation possible.