Menu

✕

June 2, 2026>Board360

KEY DATE: OBBBA provisions become testable in REG and TCP from July 1, 2026. FAR, AUD, BAR, and ISC are not affected.

The One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025. It is the largest US tax legislation since the Tax Cuts and Jobs Act (TCJA) of 2017. For CPA candidates, the implications are specific and time-sensitive. Only two exam sections are affected: REG and TCP. No other sections change. And OBBBA content does not appear in either section until July 1, 2026.

International

If you are sitting before that date, nothing changes for you. If you are sitting on or after July 1, you need to know exactly what is now testable and what that means for your study plan.

The OBBBA (formally H.R. 1, Public Law 119-21) was signed by President Trump on July 4, 2025. According to the IRS, it permanently extends most individual and business tax provisions of the 2017 TCJA that were set to expire after 2025. It also introduces several new provisions.

The core effect of the OBBBA for tax purposes:

The OBBBA is broad legislation with hundreds of provisions. On the CPA exam, only the provisions that fall within the existing REG and TCP blueprints are testable. Not every OBBBA provision appears on the exam.

The AICPA Board of Examiners approved a phased approach, confirmed by UWorld's official guidance. The rules are straightforward.

This phased approach gave candidates and educators lead time. The AICPA did not immediately swap in the new law. Instead, they drew a clean line: pre-July 1 tests on the old law, post-July 1 tests on the new law.

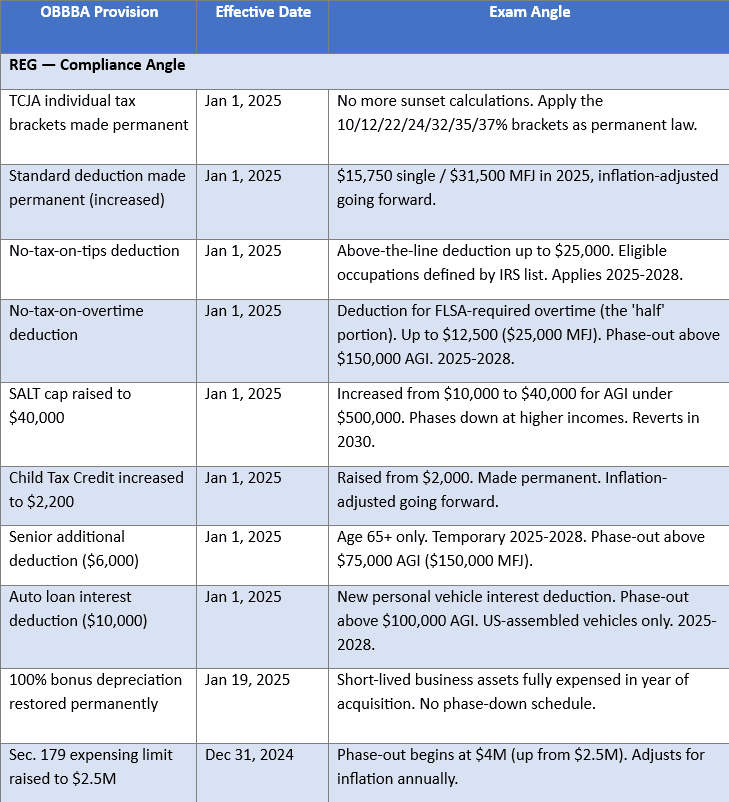

REG covers federal taxation of individuals, corporations, partnerships, and estates. It also covers business law and ethics. OBBBA hits REG on the individual and business tax sides.

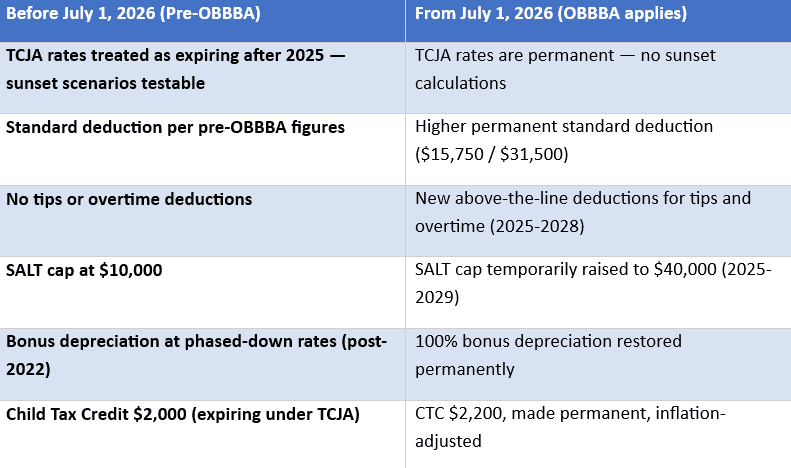

The most important conceptual shift for REG: stop preparing for TCJA sunset scenarios. Under pre-OBBBA law, candidates had to understand what would happen if TCJA provisions expired in 2025. That calculation is now irrelevant. The rates are permanent. This actually simplifies some REG content.

New content adds some complexity. The tips and overtime deductions have specific eligibility rules, phase-out thresholds, and payroll tax nuances. The SALT cap phase-out for incomes above $500,000 is a new mechanics question. These are not difficult provisions, but they need to be learned specifically.

Bonus depreciation returning to 100% also matters for REG. Pre-OBBBA, candidates studied the phase-down schedule. From July 1 onwards, it is simply 100% for qualifying assets acquired after January 19, 2025.

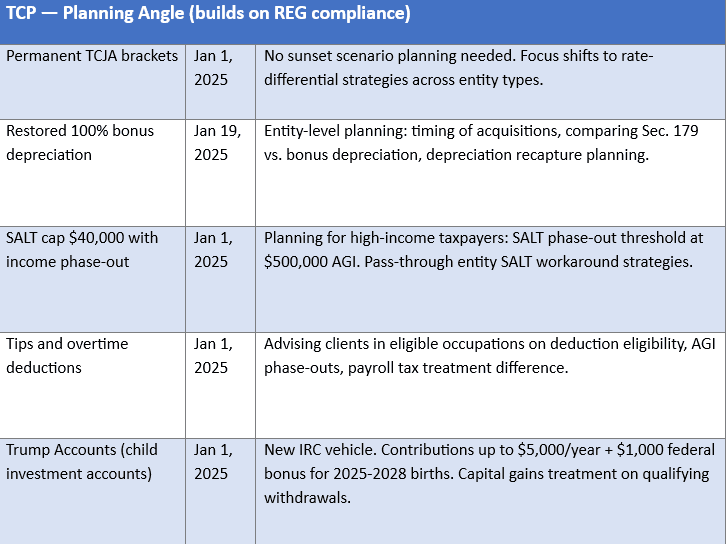

TCP goes deeper than REG. REG tests compliance mechanics. TCP tests planning judgment. OBBBA changes both angles, but TCP candidates need to think about the strategic implications of each provision, not just the rules.

Key TCP angles on OBBBA provisions:

The practical advice for TCP: do not treat OBBBA as just 'harder REG content.' The exam will ask what you would recommend to a client, not just how to calculate their tax. Keep the advisory framing in mind as you study each new provision.

Your action depends entirely on your exam date.

If you are sitting for REG or TCP before June 30, 2026:

If you are sitting for REG or TCP on or after July 1, 2026:

One important strategic point on sequencing: take REG and TCP on the same side of the July 1 cutoff. Taking REG before July 1 without OBBBA, then TCP after July 1 with OBBBA, creates unnecessary complexity. You would effectively study two different bodies of law for the two most closely related exam sections. If you cannot sit for both before the deadline, commit fully to the post-July 1 version and study both sections together under OBBBA law.

If you are evaluating the CPA as a credential and have not started yet, the OBBBA update is relevant context, not a deterrent.

The law change does not make the exam harder in net terms. Several OBBBA provisions actually simplify REG content by eliminating dual-scenario planning questions around TCJA expiry. The new provisions (tips, overtime, Trump Accounts) add specific topics, but they are narrowly defined and learnable.

If you are considering the CPA for roles in MNCs, Big 4 GCCs, or any firm that handles US tax compliance, starting sooner has value. Your study materials and program should automatically reflect the July 1 transition, so you do not have to manage the switchover yourself.

Board360.ai's CPA program is powered by UWorld, which has confirmed it is updating course materials to reflect OBBBA changes for the July 1, 2026 cutoff. That means your preparation will align with the correct testing window regardless of when you start.

Board360.ai's US CPA program is powered by UWorld, which is actively updating its content to reflect OBBBA changes ahead of the July 1, 2026 cutoff. The program covers all four exam sections including REG and TCP, with a 94% first-attempt pass rate. A free demo is available. Explore the CPA program at Board360.ai and start your preparation with materials that will reflect the correct law for your exam date.