Menu

✕

July 8, 2026>Board360

The US CPA exam changed significantly in January 2024 under a joint initiative by the AICPA and NASBA called CPA Evolution. The exam that Indian candidates are preparing for in 2026 is structurally different from what candidates sat for in 2023. If you started researching the CPA a few years ago and are only now resuming your preparation, the format you read about then no longer applies. This post explains every material change: what was replaced, what the new sections cover, how to choose your Discipline section, and what the 2025 pass rate data tells Indian candidates about where to focus.

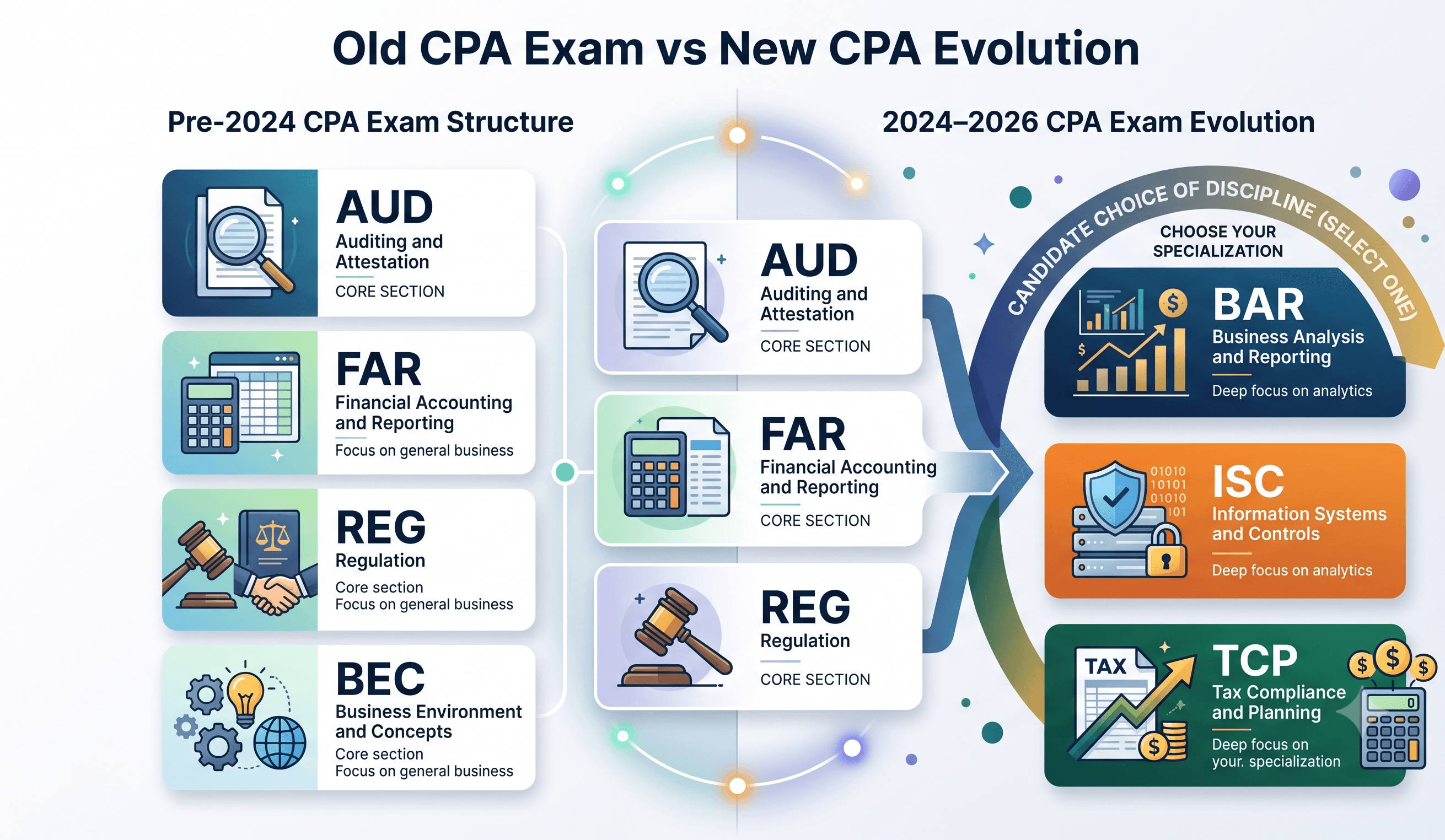

Before January 2024, the CPA exam consisted of four sections that every candidate was required to pass: Auditing and Attestation (AUD), Financial Accounting and Reporting (FAR), Regulation (REG), and Business Environment and Concepts (BEC). All four were mandatory. There was no choice involved.

The CPA Evolution model replaced this with a Core + Discipline structure. BEC was retired permanently on December 15, 2023. It was replaced by three new Discipline sections, one of which each candidate must pass. The Core sections retained the same names (AUD, FAR, REG) but their content changed.

| Factor | Old Format (Pre-2024) | New Format (2024 Onward) |

|---|---|---|

| Total Sections to Pass | 4 (all mandatory) | 4 (3 Core + 1 chosen Discipline) |

| Section Names | AUD, FAR, REG, BEC | AUD, FAR, REG + BAR, ISC, or TCP |

| Candidate Choice | None | Choose one of three Disciplines |

| Score Validity Window | 18 months | 30 months |

| Technology Content | Minimal | Tested in all 6 sections |

| BEC | Mandatory section | Retired on December 15, 2023 |

| Business Law Content | Included in BEC | Removed from the exam entirely |

| Core Testing Schedule | Quarterly windows | Continuous testing from 2025 |

| Discipline Testing Schedule | N/A | Quarterly windows |

One critical point: choosing a Discipline section does not restrict your future practice area. The AICPA is explicit on this. A CPA who passes TCP is fully licensed to practice in audit, advisory, or any other accounting function. The Discipline choice signals your specialization at the time of testing. It does not cap your career.

The Core sections carried over their names from the old format, but their content shifted. Some material moved out of Core sections into the new Discipline sections. New technology and data analytics content was added across all three.

AUD covers the fundamentals of auditing and assurance that all CPAs need regardless of specialization. The content includes audit planning, internal controls, evidence gathering, and professional standards. Technology-related audit concepts, including data analytics in audit procedures, were added to the 2024 version. Some content that previously sat in AUD relating to IT governance and business processes moved into the ISC Discipline section. AUD uses 78 multiple-choice questions (MCQs) and 7 task-based simulations (TBSs), each worth 50% of your score. The 2025 full-year pass rate was approximately 48%.

FAR covers US GAAP financial accounting and reporting for private companies, public companies, and non-profits. This is the broadest and most content-heavy Core section. Government accounting, which previously sat in FAR, has moved to the BAR Discipline section. Despite losing some content, FAR remains the section with the lowest pass rate because of the depth and breadth of GAAP knowledge required. FAR uses 50 MCQs and 7 TBSs, each worth 50% of your score. The 2025 full-year pass rate was approximately 42%.

REG covers federal tax law, ethics, and business law. Some of the more advanced tax planning content that previously sat in REG has moved to the TCP Discipline section. This has made REG more focused and, relative to the old format, less voluminous. The 2024-2025 pass rate improvement in REG reflects this reduction in scope. REG uses 72 MCQs and 8 TBSs, each worth 50% of your score. The 2025 full-year pass rate was approximately 63%.

Each candidate passes exactly one Discipline section. The three options draw on different content domains and suit different career directions. Here is what each covers.

| Section | Core Content | 2025 Pass Rate | Best Fit For |

|---|---|---|---|

| BAR | Financial statement analysis, technical accounting, business analysis, government accounting, and financial risk management | ~42% | Assurance, advisory, financial analysis, and FP&A roles |

| ISC | Information systems, IT audit, SOC engagements, cybersecurity, data governance, and internal controls over IT | ~68% | IT audit, tech-focused accounting, and systems assurance roles |

| TCP | Advanced individual taxation, entity tax planning, personal financial planning, consolidated returns, and cross-border taxation | ~78% | Tax practice, US taxation roles, and Indian CAs working with US tax teams |

BAR is the most technically demanding Discipline section by pass rate. It absorbed content from the old FAR section, including government accounting and state and local government financial reporting, and added financial analysis and business operations management content. Candidates pursuing careers in assurance, advisory services, technical accounting, or FP&A roles often choose BAR because it aligns with day-to-day work in those functions. BAR uses 50 MCQs and 7 TBSs. Its 2025 full-year pass rate was approximately 42%, the lowest among the Discipline sections. This reflects the depth of financial statement analysis and technical accounting required rather than ambiguity in the content.

ISC covers business processes, IT systems, information security, SOC engagements, cybersecurity frameworks, and IT governance. It absorbed content from the old AUD section related to IT controls and added significant new technology content that did not exist in the pre-2024 exam. The ISC scoring weight is different from other sections: 60% MCQs and 40% TBSs, versus 50/50 for all other sections.

ISC uses 82 MCQs and 6 TBSs. The 2025 full-year pass rate was approximately 68%. This is the highest-pass-rate option among the three Disciplines when accounting for the full year of 2025 data. Candidates with a technology or IT audit background, or those working in systems assurance, will find ISC content naturally familiar.

TCP covers advanced individual and entity taxation, personal financial planning, consolidated tax returns, cross-border and multijurisdictional tax issues, and transactions between entities and their owners. It absorbed complex tax planning content from the old REG section. The content overlap between REG and TCP is the primary reason TCP has the highest pass rate among all Discipline sections.

TCP uses 68 MCQs and 7 TBSs. The 2025 full-year pass rate was approximately 78%. Candidates who pass REG build directly applicable knowledge for TCP. For Indian candidates working in US tax outsourcing teams or GCCs with US tax functions, TCP is the most directly career-relevant and content-aligned Discipline choice.

The AICPA advises candidates to choose based on career direction and content fit, not pass rate. That said, pass rate is a real consideration and should be one factor in your decision alongside content alignment. Here is how to think through the choice for common Indian candidate profiles.

| Your Background or Target Role | Recommended Discipline |

|---|---|

| Working in US tax outsourcing at a Big 4, GCC, or mid-tier firm | TCP |

| Preparing Indian or NRI US tax returns | TCP |

| Working in audit or assurance at a Big 4 or mid-tier firm | BAR or ISC, depending on whether your audit work is financial or IT-focused |

| Working in FP&A, corporate finance, or management reporting | BAR |

| Working in IT audit, ERP controls, SOC reporting, or cybersecurity advisory | ISC |

| CA with no specific US work experience yet | TCP if tax-focused; BAR if accounting or finance-focused |

| B.Com or M.Com graduate targeting Big 4 US audit or advisory | BAR |

Do not choose TCP purely because its pass rate is higher. TCP's pass rate reflects that its candidate pool skews toward active tax practitioners who already know the content. A candidate with no tax background studying TCP cold will not automatically benefit from that historical pass rate.

The testing schedule changed significantly under CPA Evolution and evolved further in 2025 and 2026. Core Sections: Continuous Testing From 2025 onward, the three Core sections (AUD, FAR, REG) are available for continuous testing. There are no quarterly windows for Core sections. You can schedule and sit on almost any date that Prometric offers. Score releases for Core sections come within one to two weeks of sitting, a significant improvement from the month-plus waits of 2024.

The three Discipline sections (BAR, ISC, TCP) continue to be offered in quarterly windows. The Discipline window opens in the first month of each quarter and runs for a limited period. Score releases for Discipline sections take six to ten weeks after the testing window closes, because aggregate candidate data must be collected before scores can be released.

This scheduling difference has a practical implication: plan your Discipline exam last and time it to a quarterly window well within your 30-month score validity period. Finishing your three Core sections before sitting for the Discipline is the standard approach most candidates follow.

Under the old format, candidates had 18 months from passing their first section to pass all remaining sections. Under CPA Evolution, this window extended to 30 months. This is a meaningful improvement for Indian working professionals who cannot always dedicate full time to exam preparation.

The 30-month clock starts from the date you pass your first section. Once that clock starts, you must pass all remaining sections within 30 months. If you miss the window on any section, you lose credit for the oldest passing score and must retake and repay for that section.

The practical planning implication: do not spread your exam attempts across the full 30 months just because the window exists. Candidates who complete all four sections within 12 to 18 months minimize both the risk of score expiry and the risk of tax law changes affecting REG and TCP content between their first and last exams.

The AICPA is explicit that its scoring methodology ensures the exam is not harder or easier at different times and that pass rate increases reflect better-prepared candidates rather than an easier exam. That said, there are structural changes that affect difficulty in practice.

BAR emerged as the most difficult section of the new exam, with pass rates falling below 40% in late 2024. The section demands a level of financial analysis and technical accounting depth that many candidates did not anticipate. FAR and BAR together consistently post the lowest pass rates among all six sections in 2025.

The addition of technology and data analytics content across all sections is a genuine new demand. Indian candidates with strong traditional accounting backgrounds will need to spend deliberate time on data concepts, internal control frameworks over technology, and digital tools in accounting practice.

REG's pass rate actually improved under CPA Evolution, rising from approximately 58% in 2023 to 63% in 2025. The shift of complex tax planning content into TCP made REG more focused and proportionally more manageable for candidates who prepare specifically for what remains.

Board360 offers a US CPA program built for the CPA Evolution format, powered by UWorld with SmartPath adaptive technology. The program covers all three Core sections and all three Discipline sections so you can make an informed choice and prepare comprehensively. Explore the Board360 CPA program and book a free demo session.